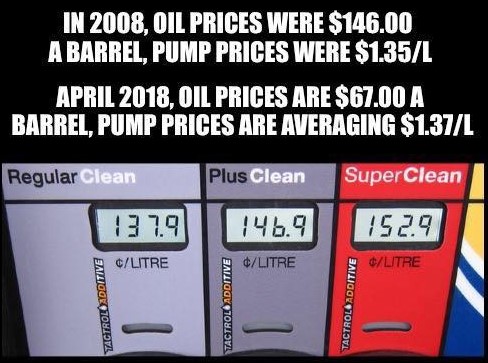

I am quite sure we are all somewhat familiar with a meme circulating social media, but just in case you have not come by it yet I am sharing it with you below.

While the image does a good enough job in getting a reaction out of the viewer, and illustrates the impact of local and federal taxes as well as changes to labour law (minimum wage increases), has on the price of products, it doesn’t address the fact that this is merely a consequence of the Bank of Canada’s monetary policy.

Back in July 2008 when oil traded at $150 USD per barrel, the Loonie was much higher; as a matter of fact, it was trading in the low 90 cent range against the greenback. Many people forget, that oil is priced in US dollars. Today, the Loonie is trading at 78 cents against the USD, or a 13.5% drop. A common tool many forex traders use when deciding which currencies to buy and which ones to sell is the Big Mac Index. While the index is considered rather anecdotal, it can be a good indicator of the Canadian Dollar’s value when compared to other currencies, typically, the USD. In June 2008, the Canadian Big Mac Index had a price of $4.08USD. Today, it’s price is at $5.26. Your average forex trader would say that the Canadian Dollar is undervalued against the USD today, and now would be a good time to invest in it. Yet, the numbers don’t quite show the big picture.

When you are making an investment in currency, you are in effect making an investment in purchasing power. You want to preserve your purchasing power when you want to exchange one currency for another. Given this, I compared the Big Mac Index against Canada’s GDP. In 2008, Canada’s GDP stood at $1.549 Trillion Dollars. Today, that GDP is down to $1.53 Trillion Dollars. So although the index is up, which implies greater purchasing power for the Loonie, if we compare our GDP in 2008 to the cost of big mac’s, we can afford LESS Big Mac’s with our GDP today than in 2008.

That Big Mac analogy probably gives us a better understanding of the overall rate of inflation. Much like a tank of gasoline is not simply a barrel of oil, a big mac is not just two all beef patties, special sauce, lettuce, cheese, pickles in a sesame seed bun. You have rent that’s a factored into the price, you transportation costs because everything needs to be delivered on trucks, energy costs for storing ingredients and preparing the meals in addition to local taxes, federal taxes, labour costs. All these ingredients are cooked into the price of a hamburger. The big mac doesn’t lie. The price is the price. You can see that the hamburger isn’t changing. What is changing is the costs of producing the hamburger and that is because the value of our money is going down because of high inflation.

The economic “recovery” that has everyone excited required the greatest amount of stimulus and budget deficits in history. Of course busts are normally proportionate to the booms that preceded them. After nearly a decade of stimulus, deficit spending, and low-interest rates by any mean, Canada has a lower GDP now than when the great recession began. To make matters worse, when you compare the amount of stimulus that the Government threw at the economy this time around, it dwarfs the amount of stimulus poured into the economy in the 90’s. What also is different now compared to the 90’s is debt. In Canada, we had something called balanced budgets. There was even talk of eliminating the national debt. Now Government is more indebted than ever.

The problems in this economy are not just limited to Government debt; Canadians are more indebted than ever and have lower rates of savings. Thanks to low-interest rates and “hype” around the housing “market”, incomes have been falling while spending was rising. What does this tell you? According to the arguments by economists on TV – you know the type, the guys and girls that suffix their names with “MBA” and probably went to Schulich and never ran a hot-god stand– tell us this is a good thing. Their spin is when the consumer is confident because of good job prospects, a strong economy, rainbows, unicorns, they go out and borrow money to buy things. When people are confident, they take on more debt. And when they are worried they reign everything in. They hunker down and want to save. But this argument is far from reality.

Let’s say you run into two friends of yours after a while. You ask both your friends how they are doing. One of your friends says they maxed out their credit cards, took a second home equity loan and borrowed against their RRSP. The other friend says they paid off a car loan, their mortgage, and fully funded their RRSP accounts for the year. Which friend would you say was doing great? The second person right? The second friend would be the person that sounded like the friend that is doing well. Most Canadians don’t want to be in debt. They want to pay off their debt (if they can). Paying down debt, building up savings is a sign of success. That is a sign of a good economy. Canada doesn’t have a good economy. All of our signs are flashing problem, flashing recession. Yet, everyone wants to pretend that everything is great. That is the mentality of investors, that’s the mentality of politicians, of most economists. Completely out of bounds, completely ridiculous.

There’s an expression saving for a rainy day. What does this mean? It means you don’t save when it is raining. You save when the sun is shining. The sun is shining on you when things are going well. When the economy is strong. When inflation is falling. That is when you set aside your emergency funds so that when things turn down. When it rains you got your rainy day fund. The idea that you just blow through your savings when there is sunshine and then when it rains you start saving is nonsense. You have to save when you are actually making money, not when you are out of work. That’s when you rely on your savings. The fact that Canadians are drawing down their savings now when the economy is supposed to be great says what about the state of the economy? It tells you that the economy is not great. That’s why people are not saving, that’s why people are in so much debt because they can’t make ends meet with their current income. Which is what you would have if the economy was good.

But all this should be great news for the Bank of Canada because the whole reason they have been keeping interest rates this low – if you look at all the justification used by Flaherty and Carney, to Poloz – was that inflation is too low. Consumer prices were not rising fast enough for comfort, so the Bank of Canada wanted to keep rates low just to make sure prices go up. Well, Victory! Gas prices are at an all-time record high. Thanks to the Bank of Canada’s monetary policy, Canadians have never paid higher prices to buy gas. Can they let rates go up now? Or are prices still not rising fast enough? Do they need to go even higher? This is how ridiculous their entire policy is.

Which brings us to the Bond Market. Falling bond prices are basically falling IOU’s for currency. If bonds are weak then why do you need the underlying currency? Because people use currency to buy bonds. If you aren’t buying the currency, what do you need it for? A weak currency and a weak bond market go hand in hand. I know people say rising interest rates are good for the currency, this is wrong. In theory, rising short-term interest rates are good for currency. Not rising long-term interest rates. In fact, short-term rates are rising but inflation is accelerating faster so in effect real yields in the short run are in fact still falling despite the fact that the Bank of Canada has been hesitantly increasing rates in recent quarters. But the bigger problem for the economy is that even though real yields are falling, the debtors still have to pay the nominal price, they still have to make the interest payments on their debt which is going to become increasingly difficult to do as rates continue increasing. Particularly, for the government of Canada itself. There will come a time when the Bank of Canada will have to make a choice; to fight a recession by slashing interest rates or fight inflation by raising them. It won’t be able to do both.

Which brings us to an old Wall Street adage; Sell in May and Go Away. The reason for this is that seasonally the market tends to produce better returns in the first four months of the year, January through April and then historically beginning in May and throughout the summer the market can generally go down. So the strategy behind this is to take your profits by selling stocks and bonds in May and then come back later in the year and buy back what you sold.

What investors should be doing in May, is selling some of their equity portfolio and bond portfolio in May, and say hello to the gold market. Particularly investors who have never been involved in gold before. It is not about selling stocks and bonds and going to cash. What good is it to sell your stocks or bonds into cash, if the value of the loonie falls more than the stock or bond markets? You will just end up losing even more purchasing power. The smart move is not just to sell stocks and bonds and hold cash, but to use some of that cash and buy gold. Last week, we told you why you should add Gold to your portfolio. Inflation is just about to become a major problem for the Bank of Canada as well as consumers. Now is the time to save for a rainy day by protecting your assets with Gold.

0 Comments